Yearly or two, the market fingers you a present wrapped in nervousness. You watch your portfolio bleed, you refresh your brokerage app greater than it’s best to, and you’re feeling helpless. However when you’ve gotten kids, that helplessness can flip into one thing extra actionable.

This previous 12 months, with the inventory market getting crunched by geopolitical turmoil, I made a decision to do one thing defiant: I invested greater than the annual present tax exclusion restrict into my kids’s custodial funding accounts.

I’ve been contributing the present tax exclusion restrict to those accounts (529 plan + custodial) since my children had been born. It’s considered one of my favourite wealth-reducing strikes, and one I’ve written about extensively right here at Monetary Samurai.

The cash goes in, it compounds, and sometime my kids can have a significant monetary security web. However this 12 months, when their portfolios had dipped, I stored going after the preliminary $19,000 contribution. By the point I used to be finished, I had contributed nearer to $35,000 per little one.

Was it probably the most tax-efficient transfer? Possibly not on paper. However it felt like the proper option to combat again towards a market I had no management over. I figured there was no want for everyone’s funds to undergo. From a proportion perspective, contributing $35,000 to a $135,000 account was much more significant than contributing to my account. That felt good, as I am at all times desirous about taking motion.

And admittedly, for many People, exceeding the present tax restrict isn’t practically as scary or sophisticated because it sounds.

What the Reward Tax Restrict Truly Means

The annual present tax exclusion is $19,000 per recipient in 2026. It tends to go up $500 to $1,000 yearly or two to account for inflation. That is the utmost you can provide a single individual with out having to report it to the IRS. Discover the phrase “report,” not “pay.” These two issues are utterly completely different, and conflating them is the place most individuals go improper.

Exceeding the annual present tax exclusion doesn’t imply you need to pay a present tax. It simply means it’s worthwhile to submit IRS Type 709 to reveal the present on what is named a present tax return. The quantity of your contribution that exceeds the annual restrict will then be subtracted out of your bigger lifetime present tax exclusion.

That lifetime exclusion is gigantic. The property and present tax exemption is $15 million per particular person for 2026, up from $13.99 million in 2025. This implies a married couple can defend a complete of $30 million with out paying any federal property or present tax. Until you might be within the rarefied territory of multimillionaire generational wealth transfers, the percentages that you’ll ever write an precise examine to the IRS for present tax are extraordinarily low.

Additional, even in the event you had been headed towards dying with an property larger than the property tax restrict, you possibly can give you a spending plan to spend down your wealth till it is proper beneath the restrict. None of us are zombies who do not act rationally to maximise wealth and reduce taxes.

After I contributed $35,000 to every of my kids’s accounts this 12 months, the portion above $19,000, which was $16,000 per little one, will depend towards my lifetime exemption. That’s $32,000 complete shaved off a $15 million wall. The wall was barely chipped.

What You Truly Should Do: File Type 709

On or earlier than April 15 of the calendar 12 months following the 12 months wherein a present is made, the person making the present should file a present tax return, Form 709, United States Reward and Technology-Skipping Switch Tax Return, if the whole worth of items given to no less than one individual aside from a partner is greater than the annual exclusion quantity for the 12 months.

So sure, I shall be submitting Type 709 subsequent tax season. It’s a comparatively easy doc. You disclose the present, calculate the overage above the annual restrict, and report how a lot of your lifetime exemption you might be utilizing. No examine written to the IRS, no penalty, no drama. You merely doc what you probably did in order that the federal government can monitor your cumulative items over your lifetime.

Type 709 is due April 15 of the next 12 months, with extensions obtainable in the event you lengthen your revenue tax return. For those who use DIY tax software program or a CPA to file your taxes, ask them so as to add Type 709 to your return. Most tax professionals deal with this routinely.

One factor married {couples} ought to know: married {couples} can mix their exclusions to surrender to $38,000 per recipient tax-free. If my partner and I had coordinated the contribution and elected present splitting, we might have given every little one $38,000 earlier than Type 709 was even required. That may be a significant quantity for folks who need to be aggressive about funding custodial accounts or 529 plans.

What Is the Likelihood You Face a Penalty If You Do not File Type 709?

Right here is the place it will get fascinating. For those who go over the annual present tax restrict and fail to file Type 709, what truly occurs?

Submitting Type 709 late when tax is owed leads to a 5% per 30 days failure-to-file penalty, as much as 25% of the unpaid tax. A separate 0.5% per 30 days failure-to-pay penalty applies to unpaid balances. But when no present tax is owed, there’s usually no financial penalty.

Learn that once more. The penalty is calculated as a proportion of the present tax owed, not the present quantity itself. For those who owe zero present tax, which you virtually definitely do except your cumulative lifetime items are north of $15 million per individual, the mathematical penalty is zero {dollars}. If no present tax is due, the 5% per 30 days penalty for failure to file Type 709 calculates to zero, as a result of the penalty is predicated on the tax due, not on the present quantity itself.

That mentioned, I’d not advocate skipping the submitting simply because the monetary penalty is technically zero. By submitting a present tax return when due, the three-year statute of limitations begins to run, and the taxpayer has closure with respect to the present transaction. This implies the IRS has three years from the date the return was filed to audit it and query the worth.

For those who by no means file, that window by no means closes. The very last thing you need is an property legal professional coping with an ambiguous present tax historical past in your behalf many years from now while you can’t reply questions your self.

How Would the IRS Even Know You Went Over The Reward Tax Restrict?

That is the query everybody thinks however not often asks out loud. The sincere reply is: for money transfers right into a custodial brokerage account, they most likely wouldn’t know except you inform them on Type 709.

Custodial accounts will not be flagged to the IRS while you make a deposit. Your brokerage isn’t submitting a type saying, “This individual simply put $35,000 into their kid’s UGMA account.” Banks do file Foreign money Transaction Studies for money deposits over $10,000, however that may be a completely different mechanism geared toward cash laundering, not present tax compliance.

A wire or ACH switch between your accounts doesn’t mechanically set off a present tax inquiry.

The present tax is essentially a self-reporting system constructed on the consideration precept and the long-term accounting of your property. The IRS trusts that folks will report giant items as a result of the system is designed to catch them at demise, not throughout life.

However by then, you are useless. What a ache within the bum for the IRS to attempt to go after your property on this scenario.

Does It Even Matter If Your Property Is Beneath the Property Tax Threshold?

For a lot of of my readers, that is probably the most virtually vital query. For those who plan to die with an property value lower than $15 million as a person or $30 million as a married couple (in right now’s {dollars} and limitations), does it matter that you just went over the annual present tax restrict?

Financially, the reply is nearly definitely no. The annual present tax exclusion and the lifetime exemption are a part of the identical unified system. Going over the annual restrict merely means you might be drawing down your lifetime exemption a bit sooner. In case your property won’t ever come near that threshold, that is purely an accounting train on Type 709. No tax will ever be owed.

The one state of affairs the place this issues extra is that if property tax legal guidelines change dramatically sooner or later and exemption limits drop.

There have been legislative proposals over time to scale back the lifetime exemption considerably, say from $15 million per individual all the way down to $5 million. If that ever occurs, your beforehand reported items would issue into the calculation. That is one more reason why submitting Type 709 and retaining good data advantages you long run, even when it feels pointless proper now.

The Actual Level of All This

My choice to contribute $35,000 per little one this 12 months was not primarily a tax technique. It was an emotional one. The market was down. My kids’s portfolios had been smaller. I wished to do one thing a couple of suboptimal scenario. Given I had the money and the conviction that issues would ultimately recuperate, I took motion.

I continually stay in two timelines to construct wealth. The primary timeline is determining make investments my capital right now to construct larger wealth sooner or later. The second timeline is continually making an attempt to anticipate the longer term, whether or not or not it’s how a lot wealth we would have in order to spend kind of right now, or how troublesome or simple life shall be for my kids, and the way a lot we have to save and make investments for them.

Sadly, I view life for all our youngsters as being tougher sooner or later as a result of AI taking on the overwhelming majority of data jobs. In the meantime, the price of dwelling will possible proceed to extend with the relentless rise in inflation of products and providers, particularly housing.

I’m sure our youngsters in 20 years will suppose we’re bozos if we did not make investments extra right now, after we had the possibility. Since I do not need to appear like a bozo to them, I am investing aggressively. Please no less than get impartial actual property by proudly owning your major house. If not for your self, to your kids.

The $500,000 Custodial Account Objective: What It Truly Takes

Mannequin out how a lot it’s worthwhile to make investments and earn to give you your custodial funding account goal. It’s a helpful and invigorating train that provides you extra goal to earn.

I’ve a particular goal for every of my kids’s custodial accounts: $500,000 by the point they graduate faculty at round age 23. It’s a quantity large enough to present them real optionality in life, however not sufficient to do nothing. Whether or not they use it to begin a enterprise, purchase a primary property, discover the world for a 12 months, maintain a progressive incapacity, or just let it maintain compounding whereas they determine issues out, half one million {dollars} at 23 is a significant basis.

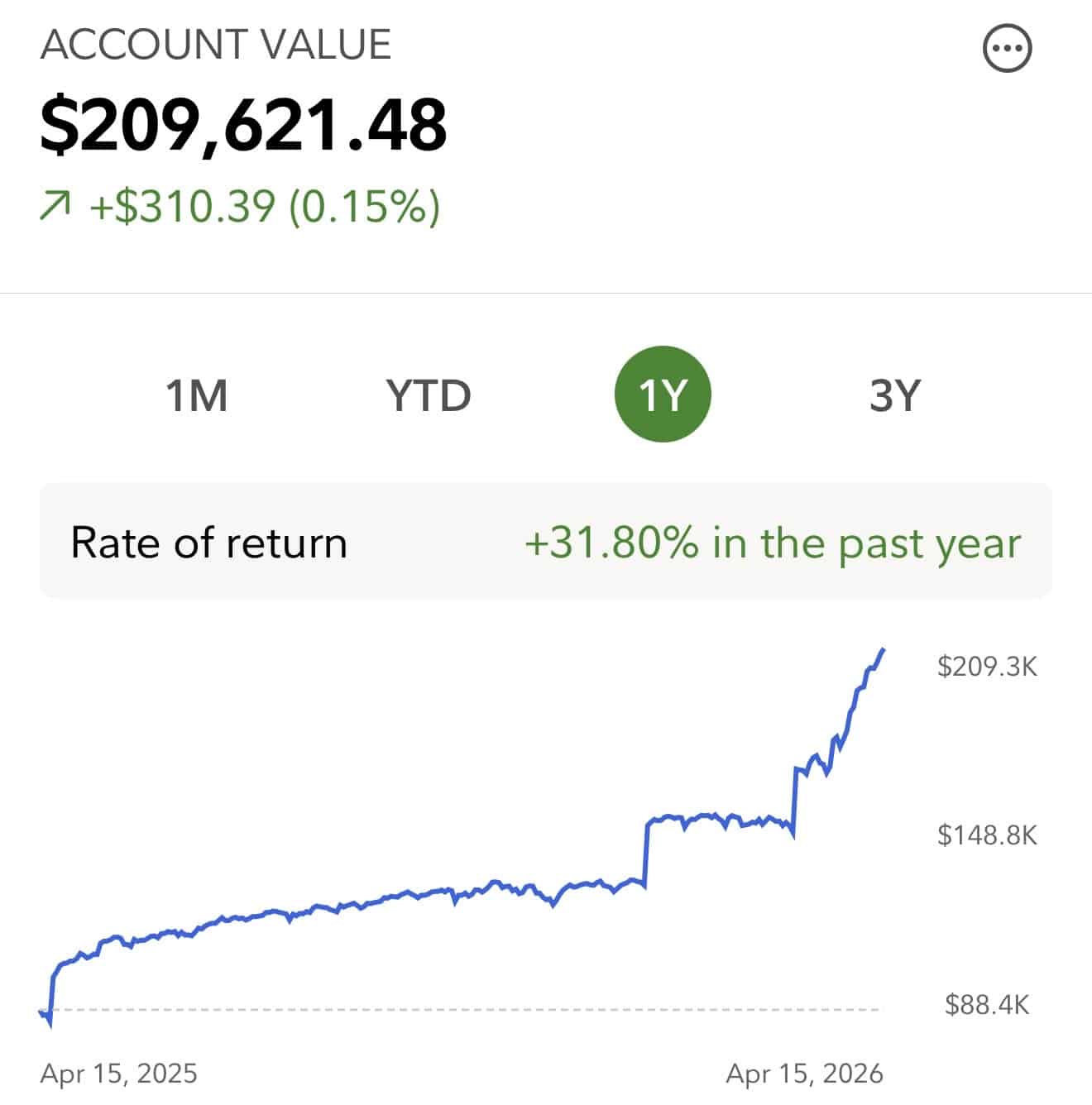

My children are presently 6 and 9. Which means I’ve roughly 17 years for my youthful little one and 14 years for my older one to hit the goal. Initially of 2026, their custodial funding accounts had balances of round $135,000. Subsequently, the compounding math is definitely fairly encouraging.

Assuming a 7% common annual return, which is an affordable long-term expectation for a diversified fairness portfolio and is under the S&P 500’s historic common, my older little one wants a contribution of roughly $9,400 per 12 months to succeed in $500,000 at commencement. That’s comfortably under the $19,000 annual present tax restrict, which implies I can do it with zero further paperwork.

My youthful little one, with three further years of runway, wants even much less, round $6,700 per 12 months, as a result of compounding does extra of the heavy lifting.

Entrance Loading the Custodial Funding Accounts Helps

What this train makes clear is that the $135,000 already in every account is doing huge work. Greater than half of the ultimate $500,000 goal will come from development on capital that’s already invested, not from future contributions. That is extraordinarily useful to know as you become old and fewer motivated to work. Beginning early and contributing constantly issues a lot greater than the precise greenback quantity in any given 12 months.

It additionally reframes what I did this 12 months by investing $35,000 per little one. The surplus $16,000 above the present tax restrict was not reckless. It was front-loading future compounding at a second when costs had been depressed. Each upward tick within the S&P 500 I envision as a prepare that leaves our children farther and farther behind. Typically, the prepare breaks down and it is time to hop on board by investing.

The purpose is to not obsess over hitting precisely $500,000. Markets can have up years and down years, and the actual quantity at commencement is likely to be $300,000 or $700,000 relying on the sequence of returns.

The purpose is to construct a disciplined system: contribute constantly, spend money on low-cost index funds, keep the course by way of downturns, and infrequently be aggressive when the market fingers you a chance. The remainder largely takes care of itself.

This is similar philosophy as constantly maxing out your 401(okay). Over a 10-year interval, I am fairly certain you may be shocked at how rather more cash you’ve gotten than you thought you’d.

The Function of Reward Tax Guidelines

The present tax guidelines exist to stop rich households from quietly transferring huge fortunes throughout generations with out paying property taxes. They weren’t designed to penalize a mum or dad who acquired a bit aggressive funding their kids’s custodial accounts throughout a market downturn. The system has a $15 million lifetime exemption exactly as a result of Congress wished extraordinary generational wealth transfers to move freely.

So if you end up in an identical place, tempted to take a position greater than $19,000 into your kid’s account as a result of the market handed you a uncommon alternative, don’t let the phrases “present tax” cease you.

File Type 709 the next April, doc your lifetime exemption utilization, and transfer on. The bureaucratic price of exceeding the annual restrict is a single further tax type. The monetary profit, shopping for extra shares at a reduction inside an account designed to compound over many years, may very well be value much more.

Markets will recuperate. The paperwork is manageable. Take the shot, particularly in case you are FIRE and need to decumulate wealth. With years of compounding forward to your kids, investing aggressively for them whereas they’re nonetheless younger is a no brainer.

Readers, are you aggressively gifting your kids and family members the present tax restrict annually or extra? For those who’ve modeled out that your web value will proceed to develop in retirement, is not the most effective decumulation methods to aggressively present to your kids and family members greater than the present tax restrict annually?

Disclaimer: As at all times, I’m not a tax skilled or monetary advisor. Please seek the advice of with a CPA or property legal professional earlier than making selections about present tax filings.

Observe Your Funds To Be In a position To Reward Higher

For those who’re constructing wealth to your kids by way of 529 plans, custodial accounts, and taxable portfolios, ensure your individual funds are optimized first.

Empower affords free monetary instruments to trace your web value, monitor money move, and analyze your investments in a single place. I’ve used their dashboard since leaving my day job in 2012, and it’s nonetheless a part of my common routine.

In case you have over $100,000 in investable property, together with financial savings, brokerage accounts, 401(okay)s, IRAs, and different accounts, you too can get a free monetary check-up with an Empower skilled. It’s a no-obligation evaluation to uncover hidden charges, allocation points, tax inefficiencies, and missed alternatives.

This is a put up sharing how my Empower free monetary evaluation went and a promotion giveaway when you full yours. A second set of eyes is at all times useful in highlighting blindspots.

In case your purpose is to construct wealth for the subsequent technology, readability issues.

{kind=link}